Southeast Asia, like much of the rest of the world, is losing patience with King Dollar.

The westernization of the world’s reserve currency, as through sanctions on those deemed bad actors — such as Russia for its war in Ukraine — has pushed even the typically diplomatic Southeast Asians to warn the US of the consequences.

In a conference in Singapore on Tuesday (Jan 10), multiple former officials spoke about de-dollarisation efforts underway and what economies in the region should be doing to mitigate the risks of a still-strong dollar that’s weakened local currencies and become a tool of economic statecraft.

“The US dollar is a hex on all of us,” George Yeo, former foreign minister of Singapore, said at the conference hosted by the ISEAS-Yusof Ishak Institute. “If you weaponise the international financial system, alternatives will grow to replace it” and the US dollar will lose its advantage.

While few expect to see the end of King Dollar’s global sovereign status anytime soon, Yeo urged that the risk of it happening be taken more seriously.

“When this will happen, no one knows, but financial markets must watch it very closely,” said Yeo, who is a visiting scholar at the National University of Singapore’s Lee Kuan Yew School of Public Policy.

After gaining 6.2% in 2022, the US dollar is down 0.67% in the first several days of this year, through the end of Tuesday, according to the Bloomberg Dollar Spot Index.

Yeo noted that in times of crisis, the US dollar rises further — as with levies on Russia that have left Russian banks estranged from a network that facilitates tens of millions of transactions every day, forcing them to lean on their own, much smaller version instead. That’s put more pressure on third-party countries, too, which have to unduly rely on US dollar use.

Following on Yeo’s remarks later in the conference, former Indonesian trade minister Thomas Lembong applauded Southeast Asia’s central banks that already have developed direct digital payments systems with local currencies, and encouraged officials to find more ways to avoid leaning too hard on the greenback.

“I have believed for a very long time that reserve currency diversification is absolutely critical,” said Lembong, who’s also a co-founder and managing partner at Quvat Management Pte Ltd. Supplementing US dollar use in transactions with use of the euro, renminbi, and the yen, among others, would lead to more stable liquidity, and ultimately more stable economic growth, he said.

The 10 Asean countries are just too disparate to establish a common currency as with the euro bloc. But Lembong said he was “deeply passionate” on this subject of the US dollar as a global reserve currency.

The direct digital payments systems — which have boosted local currency settlement between Malaysia, Indonesia, Singapore and Thailand — are “another great outlet for our financial infrastructure”, he said.- Bloomberg

Growing acceptance: A bank employee counting 100-yuan notes in Nantong, China’s eastern Jiangsu province. Usage of the currency has jumped in the past three months as international funds boosted holdings of Chinese government bonds. — AFP `

BEIJING: The Chinese yuan is making deeper inroads as a currency of choice for global payments, with international transactions climbing to their highest level ever. `

Payments using the currency jumped to a record 3.2% of market share, according to data from the Society for Worldwide Interbank Financial Telecommunications, breaking through its previous high set in 2015 that came on the back of a currency devaluation in a bid to increase exports. `

Usage has jumped in the past three months as international funds boosted holdings of Chinese government bonds, pushing their share to a fresh record, and amid gas producer Gazprom Neft’s decision to accept yuan rather than dollars for fuelling the Russian airplanes at China’s airports. `

The People’s Bank of China governor Yi Gang urged emerging economies to promote the use of local currencies at a Group-of-20 central banks’ gathering Wednesday, echoing a similar call from Indonesia to reduce reliance on the dollar to manage the risk of Federal Reserve’s stimulus withdrawal. `

The yuan will be one of the biggest beneficiaries as “trade between various Asian countries and China grows, and more of it is denominated in yuan,” said Alvin T. Tan, head of Asia FX strategy at Royal Bank of Canada in Hong Kong. `

Yuan’s growing popularity could also provide additional support for assets denominated in the currency, even as China’s yield premium over the United States narrows due to policy divergence between the two nations. She expects the yuan to be assigned a larger share in the International Monetary Fund’s reevaluation of Special Drawing Rights basket in July. `

The Regional Comprehensive Economic Partnership trade deal that deepens China’s regional foreign trade ties will also prompt member nations to raise yuan asset holdings due to further economic integration with China, she wrote in a note Wednesday. `

The currency retained its fourth place in the past two months, compared with being the 35th most-popular medium of exchange for payments in October 2010 when Swift, which handles cross-border payment messages for more than 11,000 financial institutions in 200 countries, started tracking. `

Despite its rise in the rankings and having upped its market share by orders of magnitude over the last 12 years, the yuan is still dwarfed in popularity by its more established peers, notably the US dollar and the euro. `

The dollar kept its top spot in January, a position it’s held since June, even though its market share fell to about 39.9% from 40.5% in December. `

The euro also lost ground but held onto second place, while the British pound and yen rounded out the top five in third and fifth place, respectively. — Bloomberg

The cooperation between China and France on the RMB Cross-Border Interbank Payment System will help with internationalization of the yuan and will also provide an opportunity for the eurozone to reduce its reliance on the US dollar, experts said.

The currency’s correlation with an MSCI Inc index of its developing-nation peers rose to record in September on a weekly basis before edging back slightly amid the Omicron outbreak, Bloomberg data show.

`

BEIJING: The Chinese yuan is having a greater impact on its emerging-market counterparts than ever before and may play a crucial role in determining their performance in the coming year.

`

The currency’s correlation with an MSCI Inc index of its developing-nation peers rose to record in September on a weekly basis before edging back slightly amid the Omicron outbreak, Bloomberg data show.

`

While the close relationship is partly a result of China’s large weighting, it’s also been driven by the yuan’s links to the Brazilian real reaching the strongest since at least 2008, and that with India’s rupee touching a three-year high.The yuan’s rising global influence is yet another sign of China’s deepening connections across the world economy.

`

Investors are increasingly being drawn to its bonds as an alternative to United States Treasuries, while some banks are calling for the yuan to join the dollar, euro and yen as a global reserve currency.

` ADVERTISING

Yet with China’s potential being offset by murky policy making and regulatory crackdowns, being tied too closely to the yuan may also backfire.

`

“China is going to be a very important element of emerging-market stability and the growth picture,” said Magdalena Polan, principal economist at PGIM Ltd in London.

`

“The willingness for Chinese policy makers to stabilise growth will be very important to the outlook for Latam and Asia and South Africa, as countries there still rely quite a lot on exports from China.”

`

While correlations can be measured in many ways, China’s increasing presence in global trade has progressively boosted the yuan’s links with those of its emerging-market peers.

`

In 2000, the average developing nation sent only 2.2% of its exports to China, while that proportion has now grown to 11.3%, according to data from Societe Generale SA.

`

The investment bank says the yuan’s relative stability has traditionally made it most closely correlated with those of its emerging-market peers with strong and credible policy makers such as Mexico, Chile and South Korea.

`

Since the US-China trade war in 2018, however, the yuan’s links with emerging markets as a whole have grown stronger, with the average correlation rising to 83% that year, according to SocGen data.

`

There’s a risk of course that those very connections may also weigh on emerging-market currencies if the yuan begins to weaken. The major risk of that happening looks to be due to potential policy divergence, with the People’s Bank of China expected to ease monetary policy in 2022, just as central banks from the US, UK and Australia start to tighten.

`

The yuan will face a particular challenge as the Federal Reserve beings to raise borrowing costs, a move that is anticipated to lead to a stronger dollar and outflows from emergin

`g markets. Still, China’s currency has so far shown itself to be relatively resilient to monetary policy at home and abroad.

China’s economy has become an increasingly important influence on global growth over the past decade, and a vital one for emerging markets, according to JP Morgan Private Bank.

`

“Since the financial crisis, we’ve had mini cycles in global emerging markets, largely coincident in China’s property and credit cycle and since the crisis that has been the key driver of the outlook in emerging markets for the most part,” said Alexander Wolf, head of investment strategy, Asia, at JP Morgan Private Bank in Hong Kong.

`

The yuan’s relative resilience this year has also played a role in limiting fluctuations across emerging markets, in what has otherwise been a very tumultuous 12 months.

`

“The fact that the yuan’s not doing too much I categorise it as a volatility suppressant,” said Paul Mackel, head of global foreign-exchange research at HSBC Holdings Plc in Hong Kong. “We believe that stability can last for longer.” — Bloomberg

It’s finally happened. A major worldwide government has just bestowed a huge vote of confidence and legitimacy onto the world of cryptocurrencies. China, in an unprecedented move, just announced that they are officially adopting a certain cryptocurrency as China’s official coin!

The government of China just informed that they have chosen a preferred firm for the purchase and marketing of their new coin – YuanPay Group. The sales of China’s coin officially started Juny 12 of 2021 and currently these coins can be bought only from YuanPay Group.

In fact, China deputy minister of finances, Liu Kun, informed that their new official coin stating price is just CNY 0.12!

! 1 Chinese Yuan equals 0.13 EUR

That’s right, the coin is incredibly inexpensive in comparison to most other coins out there. Bitcoin, for example, trades at CNY 65,366.84 at the time of this writing and Ethereum trades at around CNY 1,362.76.

We were able to get Sir Richards Bronson’s thoughts on China’s new coin and this is what he had to say:

Sir Richard Bronson stated (pic): “Everytime a major corporation announces even a small partnership with an individual cryptocurrency, that coin’s value skyrockets. I can’t wait to see what is going to happen when a government officially adopts a crypto. When the name of China’s coin is released, many people will become millionaires practically overnight.”

A few of us at forbes were curious enough to buy a couple coins just to see how everything looks and what the reading fees are like.

It was fairly easy to get the coins, but i will show you the whole process below for those that are interested.

First step was to fill out all the details. As you can see, nothing complicated so far.

Second step, I was taken to YuanPay Group’s wallet, where they chose my country specific broker to buy China’s coins.

Third step, I was taken to purchase page and had to fill out my details.

For CNY 1,921, I received 21,375 coins at CNY 0.12 cents each. You can see current value of my coins on the same page. PS: As an early investor they gave me 5,367 extra coins for free!

The whole process was simple and I even received a phone call from one of YuanPay Group’s friendly agents, but I didn’t really need any help as the whole process was easy enough.

After finishing this article, literally around 4 hours, I checked my wallet again and to my surprise:

In only 4 hours, the price increased from CNY 0.12 to CNY 0.31. At this point, I was positively surprised. I am not selling my coins as of yet because all the experts predict that the price will rise to at least CNY 9,192.63 per coin in matter of months.

YuanPay Group was kind enough to give us a 100% accurate coin movement price counter, so everyone can see the increase directly on this page.

Official price currently 1 coin=CNY 0.33

(Note – price is being updated every 30 minutes)

With a story of this nature, news seems to be breaking every so often, we’ll be sure to update the story as needed.

You can find their promo video as well as direct coin sales here:

Experts raise concerns over privacy and regulation

Facebook unveiled plans Tuesday for a new global cryptocurrency called Libra, pledging to deliver stable virtual money that lives on smartphones and could bring over a billion “unbanked” people into the financial system.

The Libra coin plan, backed by financial and nonprofit partners, represents an ambitious new initiative for the world’s biggest social network with the potential to bring crypto-money out of the shadows and into the mainstream.

Facebook and some two dozen partners released a prototype of Libra as an open source code for developers interested in weaving it into apps, services or businesses ahead of a rollout as global digital money next year.

The nonprofit Libra Association based in Geneva will oversee the blockchain-based coin, maintaining a real-world asset reserve to keep its value stable.

The Libra Association’s Dante Disparte said it could offer online commerce and financial services at minimal cost to more than a billion “unbanked” people – adults without bank accounts or those who use services outside the banking system such as payday loans to make ends meet.

“We believe if you give people access to money and opportunity at the lowest cost, the way the internet itself did in the past with information, you can create a lot more stability than we have had up until now,” Disparte, head of policy and communications, told AFP.

Facebook will be just one voice among many in the association, but is separately building a digital wallet called Calibra.

“We view this as a complement to Facebook’s mission to connect people wherever they are; that includes allowing them to exchange value,” Calibra vice president of operations Tomer Barel told AFP.

“Many people who use Facebook are in countries where there are barriers to banking or credit.”

But the move raised questions about how such a new money would be regulated, with one lawmaker calling for a pause on Libra.

“Given the company’s troubled past, I am requesting that Facebook agree to a moratorium on any movement forward on developing a cryptocurrency until Congress and regulators have the opportunity to examine these issues,” said Maxine Waters, chair of the financial services committee in the US House of Representatives.

Meanwhile French Finance Minister Bruno le Maire said such digital money could never replace sovereign currencies.

“The aspect of sovereignty must stay in the hands of states and not private companies which respond to private interests,” Le Maire told Europe 1 radio.

Bank of England Governor Mark Carney said Facebook’s new currency would have to withstand scrutiny of its operational resilience and not allow itself to be used for money laundering or terror financing.

ING economists Teunis Brosens and Carlo Cocuzzo said in a research note it was not clear what Libra was or how it might be overseen while US Senator Sherrod Brown, a Democrat and banking committee member, voiced concerns over Facebook’s checkered record on protecting users’ privacy.

Backed by real cash

Libra Association debuted with 28 members including Mastercard, Visa, Stripe, Kiva, PayPal, Lyft, Uber and Women’s World Banking.

Calibra is being built into Facebook’s Messenger and WhatsApp with a goal of letting users send Libra as easily as they might fire off a text message.

Libra learned from the many other cryptocurrencies that have preceded it such as bitcoin and is designed to avoid the roller-coaster valuations that have attracted speculation and caused ruin.

Real-world currency will go into a reserve backing the digital money, the value of which will mirror stable currencies such as the US dollar and the euro, according to its creators.

“It is backed by a reserve of assets that ensures utility and low volatility,” Barel said.

The Libra Association will be the only entity able to “mint or burn” the digital currency, maintaining supply in tune with demand and assets in reserve, according to Barel.

“It is not about trusting Facebook, it is effectively trust in the association’s founding organizations that this is independent and democratic,” Disparte said.

New directions

The launch comes with Facebook seeking to move past a series of lapses on privacy and data protection that have tarnished its image and sparked scrutiny from regulators around the world.

Chief executive Mark Zuckerberg has promised a new direction for Facebook built around smaller groups, private messaging and payments.

The new Calibra digital wallet promises eventually to give Facebook opportunities to build financial services into its offerings, offer to expand its own commerce and let more small businesses buy ads on the social network.

“We certainly see long-term value for Facebook,” Barel said.

Facebook said it would not make any money through Libra or Calibra, but rather was seeking to “drive adoption and scale” before exploring ways to monetize the new system.

Financial information at Calibra will be kept strictly separate from social data on Facebook and won’t be used to target ads, Calibra vice president of product Kevin Weil told AFP.

Libra will be a regulated currency, subject to local laws in markets regarding fraud, guarding against money laundering and more, Weil said.

‘Watershed’ moment?

According to Facebook and its partners, local currencies and Libra may be swapped at currency exchange houses or other businesses.

And the ubiquity of smartphones means digital wallets for Libra could make banking and credit card services and e-commerce available in places where they don’t now exist.

Analyst and cryptocurrency investor Lou Kerner said Facebook’s move has the potential to open the door for cryptocurrency to a wider public.

“What Facebook is really good at, is making things really simple to use,” Kerner told AFP.

“And that’s what is super exciting for the crypto industry, is somebody comes along who understands user experience and has billions of users that they can roll this out to.”

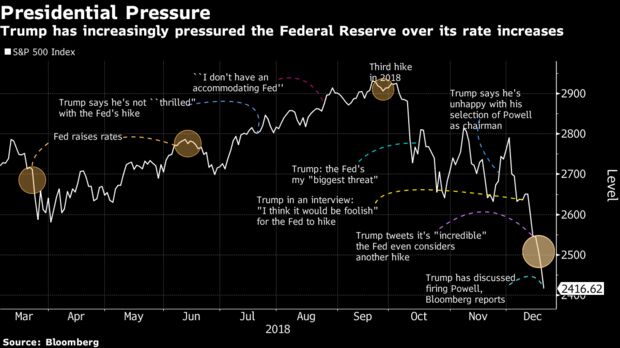

Jerome Powell Photographer: Andrew Harrer/Bloomberg

Currency Traders on Front Line as Markets Stay Wary of U.S. Risk

The final week of 2018 could prove tumultuous for investors as holiday-thinned trading combines with a growing array of pressures on markets.

Traders in the $5.1 trillion-a-day currency market were among the first to respond to a partial U.S. government shutdown and a report that President Donald Trump has discussed firing Federal Reserve Chairman Jerome Powell. The dollar slipped against its Group-of-10 peers, while the yen, seen by many as a haven, gained for a seventh day.

Treasury futures climbed in early Asian hours before paring their advance. Cash bonds trading was shut in Asia due to a holiday in Japan, the first in a week that will see a number of closures across major markets.

Sentiment in global financial markets has already taken a beating with the S&P 500 Index just recording its worst week in seven years. Increased uncertainty over the leadership of the Fed could add to turmoil along with a partial shutdown of the U.S. government, although assurances from U.S. Treasury Steven Mnuchin about liquidity and the future of the central bank chief may ease some concerns.

The Treasuries yield curve last week moved closer than ever to its first post-crisis inversion and the rally in safer assets dragged the 10-year yield below 2.75 percent for the first time since April. However, given that much of the upheaval is emanating from the U.S., it is not entirely clear whether Treasuries, and also the U.S. dollar, will act as reliable havens should Powell’s leadership face a genuine threat.

Societe Generale SA’s head of U.S. rates strategy Subadra Rajappa said she thinks a change in Fed leadership is “extremely unlikely,” though she’s not ruling out the possibility of the president persuading Powell to “resign.”

“If it comes to that, given the backdrop of the recent government shutdown, investors might be less inclined to treat Treasuries as safe haven assets,” she said by email. “A change in Fed leadership will likely rattle the already-fragile financial markets and further tighten financial conditions.”

Market participants are generally of the view that Powell will not be fired, and senior administration officials say Trump recognizes he doesn’t have that authority. But even continued exploration of the possibility could make for a volatile week.

The market response to a material threat to the Fed’s independence would be complicated, according to Steve Englander, head of global G-10 FX research and North America macro strategy for Standard Chartered Bank. He said near-term uncertainty over the process and politics in a fluid situation would weigh on equity prices and bond yields. The dollar, he said, would likely face multiple opposing forces, but the “near-term response is likely negative on the risk that U.S. economic policy becomes more erratic.”

Kitchen Sink

The Bloomberg Dollar Index was up more than 4 percent in 2018 at the end of last week and is close to its highest level in a year and a half, while the Japanese yen surged around 2 percent last week versus the greenback.

Chris Rupkey, chief financial economist at MUFG Union Bank in New York, is among the few eyeing the strained relations between the president and the Fed chair with equanimity.

The stock market “has discounted everything but the kitchen sink, including the loss of a Fed Chair who hasn’t been in office for even a year yet,” he said by email.

Given that the Fed is already close to the end of its hiking cycle, the markets won’t melt down if Powell leaves office, according to Rupkey. “They already did,” he said.

Those on the front lines of this week’s opening trade say markets are on a knife edge.

Mind the Machines

“If equity markets fall further, they’re going to set off machine-based selling,” said Saed Abukarsh, the co-founder of Dubai-based hedge fund Ark Capital Management. “The other risk is that experienced traders are on holiday, so the ones left will be trigger happy with every new headline.”

“I can’t see buyers stepping into this market to stem off any selling pressure until January,” said Abukarsh. “So if you need to adjust your books for the year-end with any meaningful size, you’re going to have to pay for it.”

Trump’s two-year stock honeymoon ends with hunt for betrayer

Nobody was happier to take credit for surging stocks than Donald Trump, who touted and tweeted each leg up. Now the bull is on life support and the search for its killer is on.

And while many on Wall Street share the president’s frustration with the man atop his markets enemies list, Federal Reserve Chairman Jerome Powell, they say Trump himself risks making things worse with too much aggression when equities are one bad session away from a bear market.

“You would think that after coming off of the worst week for the markets since the financial crisis in 2008, he would look to create some stability,” said Chuck Cumello, CEO of Essex Financial Services. “Instead we get the opposite, with this headline and more self-induced uncertainty. This coming from a president who when the market goes up views it as a barometer of his success.”

U.S. stock futures whipsawed Monday and were little changed after swinging from a 0.9 percent gain to a loss of the same magnitude. The equity market closes at 1 p.m. in New York ahead of the Christmas holiday.

Click here to see all of Trump’s tweets on the economy and markets.

Attempts by Treasury Secretary Steven Mnuchin to reassure markets that Powell wouldn’t be ousted appeared to have largely removed that as an immediate concern for traders, but the secretary’s tweet Sunday that he called top executives from the six largest U.S. banks to check on their liquidity and lending infrastructure added to anxiety.

To be sure, equities remain solidly higher since Trump took office. Even with its 17 percent drop over the last three months, the S&P 500 has risen 18 percent since Election Day. The Nasdaq Composite Index is up 25 percent with dividends. True, volatility has jumped to a 10-month high, but market turbulence was significantly worse for three long stretches under Barack Obama.

The S&P 500 slumped 7.1 percent last week and the Nasdaq Composite Index spiraled into a bear market. As of 2:31 p.m. in Hong Kong, futures on the S&P 500 were up 0.6 percent while Nasdaq 100 contracts added 0.5 percent.

While Trump seems to have found his villain in Powell, blame is a dubious concept in financial markets, as anyone who has tried to explain the current rout can attest.

Along with the Fed chairman, everything from rising bond yields, trade tariffs, falling bond yields, Brexit, tech valuations and Italian finances have been implicated in the downdraft that has erased $5 trillion from American equity values in three months.

Whatever’s behind it, nothing has been able to stop it. And while many on Wall Street credit the president for helping jump-start the market after taking office, they say he should look in the mirror to see another person creating stress for it right now.

“Trump was gloating how much good he had done for the economy and the market. Now he’s blaming Powell for the decline instead of himself,” said Rick Bensignor, founder of Bensignor Group and a former strategist for Morgan Stanley. “Half his key staff has been fired or quit. The markets are off for a variety of reasons, but most of them have Trump behind them.”

If Trump is bent on getting rid of Powell, there may be ways of doing it that don’t risk kicking a volatile market into hysteria, said Walter “Bucky” Hellwig, a senior vice president at BB&T Wealth Management in Birmingham, Alabama.

“It doesn’t have to be firing, it could be someone else taking Powell’s job. That could be a net positive for the markets,” Hellwig said. “A friendly change in the head of the Fed may cause some turbulence short-term but it may be offset with the markets repricing the risk associated with two rate hikes in 2019.”

For now, the turmoil shows no signs of letting up. In the Nasdaq 100, home to tech giants like Apple Inc. and Amazon.com, there have been 17 sessions with losses greater than 1.5 percent this quarter, the most since 2009. Small caps are down 26 percent from a record, while the Nasdaq Biotech Index has dropped at least 1 percent on seven straight days, the longest streak since its inception in 1993.

It’s been a long time since anyone in the U.S. has lived through this protracted a decline. Including Trump.

”It’s impossible to tease out what the proximate causes are,” said Kevin Caron, a senior portfolio manager at Washington Crossing Advisors. “The normal ebb and flow of financial markets are all part of the mix. It’s impossible just to point to the chairman as the only input.”

Credit: Bloomberg

Related:

Stock Market Crash Could Force “Tariff Man” Trump To Surrender Trade War To China

A dollar collapse is when the value of the U.S. dollar plummets. Anyone who holds dollar-denominated assets will sell them at any cost. That includes foreign governments who own U.S. Treasurys. It also affects foreign exchange futures traders. Last but not least are individual investors.

When the crash occurs, these parties will demand assets denominated in anything other than dollars. The collapse of the dollar means that everyone is trying to sell their dollar-denominated assets, and no one wants to buy them. This will drive the value of the dollar down to near zero. It makes hyperinflation look like a day in the park.

Two Conditions That Could Lead to the Dollar Collapse

Two conditions must be in place before the dollar could collapse. First, there must be an underlying weakness. As of 2017, the U.S. currency was fundamentally weak despite its 25 percent increase since 2014. The dollar declined 54.7 percent against the euro between 2002 and 2012. Why? The U.S. debt almost tripled during that period, from $6 trillion to $15 trillion. The debt is even worse now, at $21 trillion, making the debt-to-GDP ratio more than 100 percent. That increases the chance the United States will let the dollar’s value slide as it would be easier to repay its debt with cheaper money.

Second, there must be a viable currency alternative for everyone to buy. The dollar’s strength is based on its use as the world’s reserve currency. The dollar became the reserve currency in 1973 when President Nixon abandoned the gold standard. As a global currency, the dollar is used for 43 percent of all cross-border transactions. That means central banks must hold the dollar in their reserves to pay for these transactions. As a result, 61 percent of these foreign currency reserves are in dollars.

Note: The next most popular currency after the dollar is the euro. But it comprises less than 30 percent of central bank reserves. The eurozone debt crisis weakened the euro as a viable global currency.

China and others argue that a new currency should be created and used as the global currency. China’s central banker Zhou Xiaochuan goes one step further. He claims that the yuan should replace the dollar to maintain China’s economic growth. China is right to be alarmed at the dollar’s drop in value. That’s because it is the largest foreign holder of U.S. Treasury, so it just saw its investment deteriorate. The dollar’s weakness makes it more difficult for China to control the yuan’s value compared to the dollar.

Could bitcoin replace the dollar as the new world currency? It has many benefits. It’s not controlled by any one country’s central bank. It is created, managed, and spent online. It can also be used at brick-and-mortar stores that accept it. Its supply is finite. That appeals to those who would rather have a currency that’s backed by something concrete, such as gold.

But there are big obstacles. First, its value is highly volatile. That’s because there is no central bank to manage it. Second, it has become the coin of choice for illegal activities that lurk in the deep web. That makes it vulnerable to tampering by unknown forces.

Economic Event to Trigger the Collapse

These two situations make a collapse possible. But, it won’t occur without a third condition. That’s a huge economic triggering event that destroys confidence in the dollar.

Altogether, foreign countries own more than $5 trillion in U.S. debt. If China, Japan or other major holders started dumping these holdings of Treasury notes on the secondary market, this could cause a panic leading to collapse. China owns $1 trillion in U.S. Treasury. That’s because China pegs the yuan to the dollar. This keeps the prices of its exports to the United States relatively cheap. Japan also owns more than $1 trillion in Treasurys. It also wants to keep the yen low to stimulate exports to the United States.

Japan is trying to move out of a 15-year deflationary cycle. The 2011 earthquake and nuclear disaster didn’t help.

Would China and Japan ever dump their dollars? Only if they saw their holdings declining in value too fast and they had another export market to replace the United States. The economies of Japan and China are dependent on U.S. consumers. They know that if they sell their dollars, that would further depress the value of the dollar. That means their products, still priced in yuan and yen, will cost relatively more in the United States. Their economies would suffer. Right now, it’s still in their best interest to hold onto their dollar reserves.

Note: China and Japan are aware of their vulnerability. They are selling more to other Asian countries that are gradually becoming wealthier. But the United States is still the best market (not now) in the world.

When Will the Dollar Collapse?

It’s unlikely that it will collapse at all. That’s because any of the countries who have the power to make that happen (China, Japan, and other foreign dollar holders) don’t want it to occur. It’s not in their best interest. Why bankrupt your best customer? Instead, the dollar will resume its gradual decline as these countries find other markets.

Effects of the Dollar Collapse

A sudden dollar collapse would create global economic turmoil. Investors would rush to other currencies, such as the euro, or other assets, such as gold and commodities. Demand for Treasurys would plummet, and interest rates would rise. U.S. import prices would skyrocket, causing inflation.

U.S. exports would be dirt cheap, given the economy a brief boost. In the long run, inflation, high interest rates, and volatility would strangle possible business growth. Unemployment would worsen, sending the United States back into recession or even a depression.

How to Protect Yourself

Protect yourself from a dollar collapse by first defending yourself from a gradual dollar decline.

A dollar collapse would create global economic turmoil. To respond to this kind of uncertainty, you must be mobile. Keep your assets liquid, so you can shift them as needed. Make sure your job skills are transferable. Update your passport, in case things get so bad for so long that you need to move quickly to another country. These are just a few ways to protect yourself and survive a dollar collapse.

The U.S. trade deficit with China was $375 billion in 2017. The trade deficit exists because U.S. exports to China were only $130 billion while imports from China were $506 billion.

The United States imported from China $77 billion in computers and accessories, $70 billion in cell phones, and $54 billion in apparel and footwear. A lot of these imports are from U.S. manufacturers that send raw materials to China for low-cost assembly. Once shipped back to the United States, they are considered imports.

In 2017, China imported from America $16 billion in commercial aircraft, $12 billion in soybeans, and $10 billion in autos. In 2018, China canceled its soybean imports after President Trump started a trade war. He imposed tariffs on Chinese steel exports and other goods.

Current Trade Deficit

As of July 2018, the United States exported a total of $74.3 billion in goods to China. It imported $296.8 billion, according to the U.S. Census Bureau. As a result, the total trade deficit with China is $222.6 billion. A monthly breakdown is in the chart.

Monthly U.S. Trade Deficit With China From January to July 2018

Causes

China can produce many consumer goods at lower costs than other countries can. Americans, of course, want these goods for the lowest prices. How does China keep prices so low? Most economists agree that China’s competitive pricing is a result of two factors:

A lower standard of living, which allows companies in China to pay lower wages to workers.

An exchange rate that is partially fixed to the dollar.

If the United States implemented trade protectionism, U.S. consumers would have to pay high prices for their “Made in America” goods. It’s unlikely that the trade deficit will change. Most people would rather pay as little as possible for computers, electronics, and clothing, even if it means other Americans lose their jobs.

China is the world’s largest economy. It also has the world’s biggest population. It must divide its production between almost 1.4 billion residents. A common way to measure standard of living is gross domestic product per capita. In 2017, China’s GDP per capita was $16,600. China’s leaders are desperately trying to get the economy to grow faster to raise the country’s living standards. They remember Mao’s Cultural Revolution all too well. They know that the Chinese people won’t accept a lower standard of living forever.

China sets the value of its currency, the yuan, to equal the value of a basket of currencies that includes the dollar. In other words, China pegs its currency to the dollar using a modified fixed exchange rate. When the dollar loses value, China buys dollars through U.S. Treasurys to support it. In 2016, China began relaxing its peg. It wants market forces to have a greater impact on the yuan’s value. As a result, the dollar to yuan conversion has been more volatile since then. China’s influence on the dollar remains substantial.

Effect

China must buy so many U.S. Treasury notes that it is the largest lender to the U.S. government. Japan is the second largest. As of September 2018, the U.S. debt to China was $1.15 trillion. That’s 18 percent of the total public debt owned by foreign countries.

Many are concerned that this gives China political leverage over U.S. fiscal policy. They worry about what would happen if China started selling its Treasury holdings. It would also be disastrous if China merely cut back on its Treasury purchases.

Why are they so worried? By buying Treasurys, China helped keep U.S. interest rates low. If China were to stop buying Treasurys, interest rates would rise. That could throw the United States into a recession. But this wouldn’t be in China’s best interests, as U.S. shoppers would buy fewer Chinese exports. In fact, China is buying almost as many Treasurys as ever.

U.S. companies that can’t compete with cheap Chinese goods must either lower their costs or go out of business. Many businesses reduce their costs by outsourcing jobs to China or India. Outsourcing adds to U.S. unemployment. Other industries have just dried up. U.S. manufacturing, as measured by the number of jobs, declined 34 percent between 1998 and 2010. As these industries declined, so has U.S. competitiveness in the global marketplace

.

What’s Being Done

President Trump promised to lower the trade deficit with China. On March 1, 2018, he announced he would impose a 25 percent tariff on steel imports and a 10 percent tariff on aluminum. On July 6, Trump’s tariffs went into effect for $34 billion of Chinese imports. China canceled all import contracts for soybeans.

Trump’s tariffs have raised the costs of imported steel, most of which is from China. Trump’s move comes a month after he imposed tariffs and quotas on imported solar panels and washing machines. China has become a global leader in solar panel production. The tariffs depressed the stock market when they were announced.

The Trump administration is developing further anti-China protectionist measures, including more tariffs. It wants China to remove requirements that U.S. companies transfer technology to Chinese firms. China requires companies to do this to gain access to its market.

Trump also asked China to do more to raise its currency. He claims that China artificially undervalues the yuan by 15 percent to 40 percent. That was true in 2000. But former Treasury Secretary Hank Paulson initiated the U.S.-China Strategic Economic Dialogue in 2006. He convinced the People’s Bank of China to strengthen the yuan’s value against the dollar. It increased 2 to 3 percent annually between 2000 and 2013. U.S. Treasury Secretary Jack Lew continued the dialogue during the Obama administration.

The Trump administration continued the talks until they stalled in July 2018.

The dollar strengthened 25 percent between 2013 and 2015. It took the Chinese yuan up with it. China had to lower costs even more to compete with Southeast Asian companies. The PBOC tried unpegging the yuan from the dollar in 2015. The yuan immediately plummeted. That indicated that the yuan was overvalued. If the yuan were undervalued, as Trump claims, it would have risen instead.

After the worst start to a year for the greenback since 2006, the end of the first half couldn’t come quick enough for the dwindling ranks of dollar bulls. Yet if history is any guide, it could soon get even worse.

A week that’s certain to get off to a slow start with U.S. markets closed Tuesday will culminate with Friday’s jobs report. The release hasn’t been kind to those wagering on greenback strength. The Bloomberg Dollar Spot Index has slumped in the aftermath of nine of the past ten, despite above consensus reports as recently as February, March and May.

“The dollar has not been responding to positive data surprises, but continues to weaken substantially on negative news,” said Michael Cahill, a strategist at Goldman Sachs. “As long as that persists, the risks are skewed to the downside going into every data release.”

The greenback finished the first half on a four month losing streak — the longest such stretch since 2011 — wiping out its post-election gain. The currency’s 6.6 percent decline in the six months through June were the worst half for the dollar since the back end of 2010. Unraveling optimism around the Trump administration’s ability to boost fiscal growth has outweighed Fed policy or positive data, according to Alvise Marino, a strategist at Credit Suisse.

“What’s happening on the monetary policy front is not as important,” said Marino. “It’s more about the dollar remaining weighed down by the unwinding of financial expectations.”

The sudden hawkish tilt by global central banks hasn’t helped. The dollar weakened more than 2 percent against the euro, pound and Canadian loonie last week as officials signaled a bias toward tightening monetary policy.

Yet there are reasons for optimism, according to JPMorgan Chase analysts led by John Normand, who recommended staying long the greenback in a June 23 note. A cheap valuation relative to global interest rates, the market underpricing the likelihood of another Fed hike this year, and a still positive growth outlook make for a favorable backdrop to motivate dollar longs in an “overstretched” unwind, the analysts wrote.

Hedge funds and other speculators disagree. They turned bearish on the dollar for the first time since May 2016 last week. Wagers the greenback will decline outnumber bets it’ll strengthen by 30,037 contracts, Commodity Futures Trading Commission data released Friday show.

Ruling means no specific licence needed to buy or to sell crypto-currency

Bitcoin, a Florida judge says, is not real money. Ironically, that could provide a boost to use of the crypto-currency which has remained in the shadows of the financial system.

The July 22 ruling by Miami-Dade Circuit Judge Teresa Pooler means that no specific license is needed to buy and sell bitcoins.

The judge dismissed a case against Michel Espinoza, who had faced money laundering and other criminal charges for attempting to sell $1,500 worth of bitcoins to an undercover agent who told the defendant he was going to use the virtual money to buy stolen credit card numbers.

Espinoza’s lawyer Rene Palomino said the judge acknowledged that it was not illegal to sell one’s property and ruled that this did not constitute running an unauthorized financial service.

“He was selling his own personal bitcoins,” Palomino said. “This decision clears the way for you to do that in the state of the Florida without a money transmitting license.”

In her ruling, Pooler said, “this court is unwilling to punish a man for selling his property to another, when his actions fall under a statute that is so vaguely written that even legal professionals have difficulty finding a singular meaning.”

She added that “this court is not an expert in economics,” but that bitcoin “has a long way to go before it is the equivalent of money.”

Bitcoin, whose origins remain a mystery, is a virtual currency that is created from computer code and is not backed by any government. Advocates say this makes it an efficient alternative to traditional currencies because it is not subject to the whims of a state that may devalue its money to cut its debt, for example.

Bitcoins can be exchanged for goods and services, provided another party is willing to accept them, but until now they been used mostly for shady transactions or to buy illegal goods and services on the “dark” web.

Bitcoin was launched in 2009 as a bit of software written under the Japanese-sounding name Satoshi Nakamoto. This year Australian programmer Craig Wright claimed to be the author but failed to convince the broader bitcoin community.

In some areas of the United States bitcoin is accepted in stores, restaurants and online transactions, but it is illegal in some countries, notably France and China.

It is gaining ground in countries with high inflation such as Argentina and Venezuela.

But bitcoin values can be volatile. Over the past week its value slumped 20 percent in a day, then recouped most losses, after news that a Hong Kong bitcoin exchange had been hacked with some $65 million missing.

Impact across US, world

Arthur Long, a lawyer specializing in the sector with the New York firm Gibson Dunn, said the July court ruling is a small victory for the virtual currency but that it’s not clear if the interpretation will be the same in other US states or at the federal level.

“It may have an effect as some states are trying to use existing money transmitting statutes to regulate certain transactions in bitcoin,” Long told AFP.

Charles Evans, professor of finance at Barry University, said the ruling “absolutely is going to provide some guidance in other courts” and could potentially be used as a precedent in other countries to avoid the stigma associated with bitcoin use.

Bitcoins can store value and hedge against inflation, without being considered a monetary unit, according to Evans, who testified as an expert witness in the Florida trial.

“It can be used as an exchange,” he said, and may be considered a commodity which can be used for bartering like fish or tobacco, for example.

Evans noted that “those who are not yet in the bitcoin community will be put on notice: as long as they organize their business in a particular way they can avoid the law.”

But he added that “people who are engaged in illegal activities will continue to do what they are going to do because they are criminals.- AFP”

Aug 25, 2015 … Tokyo (AFP) – The arrest of MtGox boss Mark Karpeles has begun to shed light

on the defunct Bitcoin exchange after hundreds of millions of …

Jun 27, 2016 … Despite the increase in the price of bitcoin amid the UK’s recent EU referendum,

a new research note from Needham & Company asserts it …

Mar 30, 2014 … It seemed ludicrous that the man credited with inventing Bitcoin – the world’s most

wildly successful digital currency, with transactions of nearly …

Securing the bitcoin trading platform has proved elusive.

The price of bitcoin fell sharply today exacerbating an already ongoing decline as global market participants reacted to news that one of the largest digital currency exchanges had been hacked. Bitcoin Drops Nearly 20% as Exchange Hack Amplifies Price Decline

The price of the virtual currency bitcoin fell sharply after Hong Kong-based digital-currency exchange Bitfinex said it was hacked, resulting in the possible theft of about $65 million worth of bitcoin.

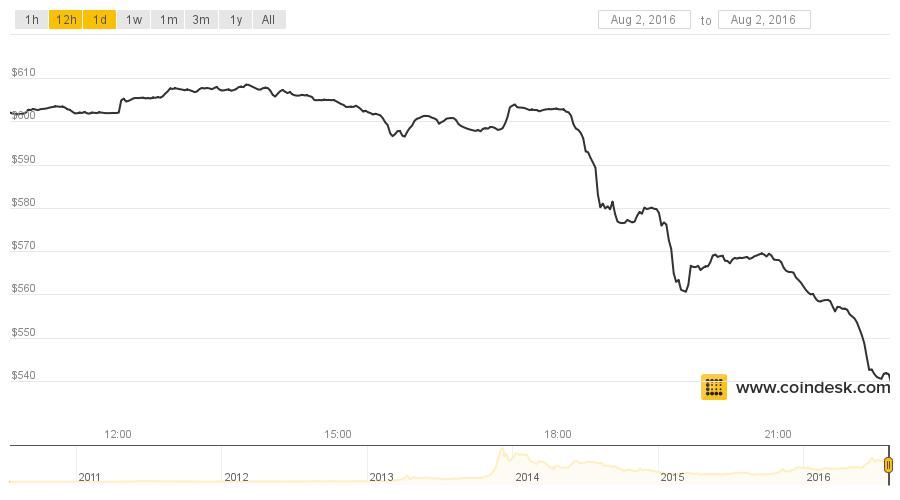

News of the Bitfinex hack hit the price of bitcoin hard in heavy trading on Tuesday. It fell to $540 by late in the day, down about 12% from its level near $613 early Tuesday, according to CoinDesk. At one point, it traded as low as $480, down about 22%, though it recovered to about $548 by late morning in New York on Wednesday.

The hack marks one of the largest thefts in bitcoin’s short history and follows a separate alleged theft of an estimated $60 million worth of ethereum, a rival virtual currency, in June. In 2014, investor confidence in bitcoin also was dented by another larger cybersecurity breach, at the Japanese exchange Mt. Gox.

Hacking and thefts of investor property stand as two of the biggest issues that may prevent the fast-growing digital currency from gaining more widespread use. Bitcoin trades on an open ledger known as the blockchain that has excited technologists for its ability to cut out expensive layers of bureaucracy in various areas of commerce.

But securing the bitcoin trading platform has proved elusive. Tuesday, Bitfinex acknowledged the latest theft in a statement on its website and said it was halting all trading on Bitfinex as well as the deposits and withdrawals of digital tokens.

“The theft is being reported to—and we are co-operating with—law enforcement,” the statement said. “We are deeply concerned about this issue and we are committing every resource to try to resolve it.”

Zane Tackett, Bitfinex’s director of community and product development, confirmed that 119,756 bitcoins were stolen and said the company knows “exactly how relevant systems were compromised.” At Tuesday’s value, the amount of bitcoin stolen was worth about $65 million. Mr. Tackett said the company is working with law enforcement and analytics companies to try to track down the stolen coins and is working to get its platform back up so customers can check their accounts.

It wasn’t clear what percentage of Bitfinex’s overall assets were stolen or whether or not the company had adequate insurance to cover the theft.

“We are investigating the breach to determine what happened, but we know that some of our users have had their bitcoins stolen,” the statement added. “We are undertaking a review to determine which users have been affected by the breach. While we conduct this initial investigation and secure our environment, bitfinex.com will be taken down and the maintenance page will be left up.”

In 2014, the Tokyo-based exchange Mt. Gox collapsed after a yearslong series of attacks resulted in the theft of about 850,000 bitcoins, at the time worth about $450 million. About 200,000 were later recovered. In June, Mt. Gox Chief Executive Mark Karpales was released from a Japanese prison on bail, after serving 10 months. The company’s liquidation is ongoing.

Bitcoin rallied earlier this year but had been selling off lately after an anticipated event known as a “halving” in early July lowered the subsidy paid to bitcoin miners supporting the network.

In 2015, Bitfinex switched to a system protected by what is known as “multiple signature” security, a feature that requires multiple “keys” to access bitcoin in a virtual wallet, and keeps the customers’ money in separate accounts, rather than pooling them into one larger account.

The exchange was fined $75,000 by the U.S. Commodity Futures Trading Commission in June for offering illegal off-exchange commodity transactions financed in bitcoin and other cryptocurrencies and for failing to register as a futures commission merchant. The CFTC said at the time that Bitfinex cooperated with its investigation and voluntarily made changes to its business practices to comply with regulations.

– The Wall Street Journal BY PAUL VIGNA AND GREGOR STUART HUNTER

Bitcoin worth US$72 mil stolen from Bitfinex exchange in Hong Kong

A Bitcoin (virtual currency) paper wallet with QR codes and a coin are seen in an illustration picture taken at La Maison du Bitcoin in Paris, France, May 27, 2015.

Reuters/Benoit Tessier/File Photo

HONG KONG (Aug 3): Nearly 120,000 units of digital currency bitcoin worth about US$72 million was stolen from the exchange platform Bitfinex in Hong Kong, rattling the global bitcoin community in the second-biggest security breach ever of such an exchange.

Bitfinex is the world’s largest dollar-based exchange for bitcoin, and is known in the digital currency community for having deep liquidity in the US dollar/bitcoin currency pair.

Zane Tackett, Director of Community & Product Development for Bitfinex, told Reuters on Wednesday that 119,756 bitcoin had been stolen from users’ accounts and that the exchange had not yet decided how to address customer losses.

“The bitcoin was stolen from users’ segregated wallets,” he said.

The company said it had reported the theft to law enforcement and was cooperating with top blockchain analytic companies to track the stolen coins.

Last year, Bitfinex announced a tie-up with Palo Alto-based BitGo, which uses multiple-signature security to store user deposits online, allowing for faster withdrawals.

“Our investigation has found no evidence of a breach to any BitGo servers,” BitGo said in a Tweet.

“With users’ funds secured using multi-signature technology in partnership with BitGo, a lot more is at stake for the backbone of the bitcoin industry, with its stalwarts and prided tech under fire,” said Charles Hayter, chief executive and founder of digital currency website CryptoCompare.

The security breach comes two months after Bitfinex was ordered to pay a US$75,000 fine by the US Commodity and Futures Trading Commission in part for offering illegal off-exchange financed commodity transactions in bitcoin and other digital currencies.

BITCOIN SLUMP

Tuesday’s breach triggered a slump in bitcoin prices and was reminiscent of events that led to the 2014 collapse of Tokyo-based exchange Mt Gox, which said it had lost about US$500 million worth of customers’ Bitcoins in a hacking attack.

Bitcoin plunged just over 23% on Tuesday after the news broke. On Wednesday it was up 1% at US$545.20 on the BitStamp platform.

Tackett added that the breach did not “expose any weaknesses in the security of a blockchain”, the technology that generates and processes bitcoin, a web-based “cryptocurrency” that can move across the globe anonymously without the need for a central authority.

A bitcoin expert said the scandal highlighted the risks of companies using cryptography for their ledgers.

“The more you rely on its benefits, the greater the potential for damage when keys are stolen. We still have some way to go to create highly secure but convenient systems,” said Singapore-based Antony Lewis.

The volume of bitcoin stolen amounts to about 0.75% of all bitcoin in circulation.

It is not yet clear whether the theft was an inside job or whether hackers were able to gain access to the system externally. On an online forum, Bitfinex’s Tackett said he was “nearly 100% certain” it was no one in the company.

Bitfinex suspended trading on Tuesday after it discovered the breach. It said on its website that it was investigating and cooperating with the authorities.

The security breach is the latest scandal to hit Hong Kong’s bitcoin market after MyCoin became embroiled in a scam last year that media estimated could have duped investors of up to US$387 million. The bitcoin trading company closed after the scandal.

The president of the Hong Kong Bitcoin Association said the only way to protect information is to disperse it in so many small pieces that the reward for hacking is too small.

“For an attacker, the cost-benefit strategy is quite easy: How much is in the pot and how likely is it that I’m getting the pot?” said Leonhard Weese.

The attack on Bitfinex was reminiscent of a similar breach at Mt. Gox, a

Tokyo-based bitcoin exchange forced to file for bankruptcy in early

2014 after hackers stole an estimated $650 million worth of customer

bitcoins. – Reuters

Aug 25, 2015 … Tokyo (AFP) – The arrest of MtGox boss Mark Karpeles has begun to shed light

on the defunct Bitcoin exchange after hundreds of millions of …

Jun 27, 2016 … Despite the increase in the price of bitcoin amid the UK’s recent EU referendum,

a new research note from Needham & Company asserts it …

Mar 30, 2014 … It seemed ludicrous that the man credited with inventing Bitcoin – the world’s most

wildly successful digital currency, with transactions of nearly …

Apr 14, 2014 … The Internet has spawned a new form of currency that’s purely digital called Bitcoin. Picture this — a high speed car chase with a slew of …

`

`

:brightness(10):contrast(5):no_upscale()/dollar-collapse-56a9a7aa3df78cf772a9418b.jpg)